Crude Prices Retreat as Hormuz Flows Continue and Refining Constraints Tighten Product Markets

July 17, 2026

July 17, 2026

WTI and Brent crude settled lower on Thursday after a volatile session driven by the risk that Houthi forces could block the Bab el-Mandeb Strait. Shipping through the Strait of Hormuz has fallen sharply but has not stopped, tempering the market’s response to the latest escalation in U.S.-Iran tensions. Attention now turns to preliminary U.S. consumer sentiment and inflation-expectations data at 10:00 a.m. ET on July 17, followed by the weekly U.S. oil rig count at 1:00 p.m. ET.

Crude Oil Market Overview

Crude Retreats After WTI Briefly Breaks Above $80

International crude prices swung sharply on Thursday as traders assessed reports that Houthi forces could close the Bab el-Mandeb Strait. WTI briefly climbed above $80 a barrel before giving up all its gains and turning lower. It settled down 1.05% at $78.88 a barrel, while Brent crude fell 0.78% to $84.02.

The retreat suggested that traders remain reluctant to price in a major geopolitical premium without clearer evidence of physical supply losses. After climbing above $107 in the spring and then falling rapidly to $67, crude has struggled to hold above key levels despite renewed military escalation between the United States and Iran.

Supply conditions have also limited the upside. U.S. crude production is near a record 13.5 million barrels per day, while output from Brazil, Guyana, and Canada continues to grow. The market still expects a possible surplus later in 2026. Weaker OPEC+ production discipline and substantial spare capacity in Saudi Arabia and other Gulf producers have reinforced expectations that adequate supply buffers remain available.

Falling Hormuz Traffic Keeps Regional Supply Risks Elevated

The United States struck Iranian coastal defenses and missile bases on Wednesday after reinstating its maritime blockade of Iranian ports. Tehran responded by threatening further disruption to regional energy exports and described the conflict with Washington as a “war of survival.” The escalation followed the breakdown of a fragile ceasefire reached in June and renewed concerns about a broader regional conflict.

Traffic through the Strait of Hormuz, which handled about one-fifth of daily global oil and liquefied natural gas trade before the war began, has declined substantially. Only seven vessels passed through the waterway on Wednesday, down from 13 on Tuesday. Commercial shipping has not stopped entirely, however, and tankers continue to transit the strait in limited numbers.

Iran said Thursday that the strait was an inviolable “red line” and would not reopen in response to U.S. pressure. It also warned that infrastructure across the Gulf could be targeted if President Donald Trump carried out threats to attack Iranian infrastructure. The Islamic Revolutionary Guard Corps said that if U.S. forces made a strategic mistake, “everyone must say goodbye to energy from this region.”

The immediate concern is therefore less about a complete loss of supply than about slower shipping flows, more cautious vessel operations, and the growing risk of a future interruption. Some shipowners have reduced their exposure to high-risk areas, adjusted routes, and strengthened security measures as military tensions have intensified.

The threat could extend beyond Hormuz. Foreign media reported that Iran had privately instructed the Houthis to close the Bab el-Mandeb Strait if the United States attacked Iranian power facilities. The Houthis also warned Saudi Arabia that all of its oil facilities would become targets if it launched another attack. The Bab el-Mandeb carries about one-tenth of global seaborne crude trade, making any prolonged disruption another potential source of pressure on energy flows.

A separate operational disruption emerged after a drone collided with a tanker. Sources said crude transfers at all Iraqi oil shipping terminals had been suspended following the incident.

Refining Constraints Raise the Risk of Persistent Product Shortages

Uncertainty surrounding global refining capacity is becoming increasingly important relative to the immediate availability of crude. Middle Eastern refining infrastructure has sustained severe damage and may not recover quickly even if hostilities stop immediately. Russia’s refining capacity has also fallen sharply during the prolonged Russia-Ukraine war and is unlikely to return to its previous peak in the near term.

JPMorgan data showed that global refinery runs have declined by 8.2 million barrels per day in 2026. This suggests that even if crude flows recover, refiners may lack sufficient capacity to process all available feedstock.

The U.S. 3:2:1 crack spread has risen steadily since the conflict began and reached a record high in mid-July. Russian diesel and fuel oil exports have fallen by about two-thirds from their peak, tightening the global distillate market. Russia is the world’s second-largest diesel exporter and accounts for about 12% of global exports, making disruptions to its refining system more consequential for refined products than for crude itself.

In the short term, restricted Hormuz flows and constrained refining capacity are leaving the refined-product supply gap unfilled. Crack spreads remain elevated, and refined products continue to outperform crude. Over the medium term, the outlook will depend on how quickly the Middle East restores 11.7 million barrels per day of refining capacity and whether Russia’s refining system can be repaired as scheduled by early 2027. If both recoveries fall short of expectations, structural tightness in refined products could keep crack spreads high and transmit more persistent price pressure through fuel costs into broader inflation.

U.S. Data and Drilling Activity Are the Next Catalysts

The United States is scheduled to release preliminary July one-year inflation expectations and the preliminary University of Michigan consumer sentiment index at 10:00 a.m. ET on July 17. The weekly U.S. oil rig count for the period through July 17 is due at 1:00 p.m. ET.

Monetary policy also remains part of the broader market backdrop. Dallas Federal Reserve President Lorie Logan, a voting member of the Federal Open Market Committee this year, said she currently believed a moderate interest-rate increase would better balance the outlook and its risks. She said modest policy tightening now would be preferable to having to tighten much more aggressively later.

Crude Oil Outlook: Global Market Views

This section reviews the main views on crude oil from global financial institutions and market participants. Each view has been summarized and restructured by the RYOEX Research Team based on publicly available information. References to any institution or individual do not imply endorsement of RYOEX or its views.

Fiona Cincotta | Escalating U.S.-Iran Tensions Keep Crude Near Monthly Highs

Senior market analyst Fiona Cincotta said crude remained near monthly highs, with WTI trading around $80 a barrel as renewed escalation between the United States and Iran continued to support prices.

Cincotta said the United States had reimposed a maritime blockade on Iranian ports the previous week, while Tehran had threatened to disrupt additional regional energy exports. Although geopolitical risk remained supportive, the market paused after a sharp rise earlier in the week. Shipping through Hormuz remained far below normal levels, while mediation efforts by neighboring countries continued.

In her view, stabilization near current prices indicated that investors had not yet priced in a full-scale regional conflict, although a significant geopolitical risk premium remained embedded in the market. If Iran used its Houthi allies to disrupt shipping through the Bab el-Mandeb, upward pressure on crude could intensify.

Looking further ahead, Cincotta said prices could remain elevated in the fourth quarter if export flows recover slowly, particularly because global inventories were already low after substantial drawdowns in the second quarter. If tensions continue to ease and daily production recovers more quickly, crude could return to the $60 range before year-end.

SEB Research | Continued Hormuz Disruption Could Lift Crude Toward $90-$100

Ole Hvalbye, a market analyst at SEB Research, said the market’s response to the escalation had remained surprisingly calm. He said crude could continue climbing to $90-$95 a barrel and might even reach $100 again because persistent disruption in the Strait of Hormuz had made Gulf oil flows increasingly uncertain.

Exness | Limited Tanker Traffic Warrants Caution Over Immediate Supply Losses

Wael Makarem, head of financial market strategy at Exness, said the market could remain cautious in assessing current supply risks. Despite intensifying military tensions, tankers were still navigating the Strait of Hormuz, although in limited numbers.

Oxford Economics | Volatile Hormuz Traffic Could Keep Average Prices Above $80

Oxford Economics said the most likely scenario was that low and volatile traffic through the Strait of Hormuz would produce intermittent oil-price spikes. Under that scenario, average crude prices could remain above $80 a barrel for several consecutive quarters.

Joshua Gibson | Physical Supply Losses Are Needed for WTI to Hold Above $80

Analyst Joshua Gibson said crude had failed to hold above $80 despite the escalation of the U.S.-Iran conflict, renewed U.S. restrictions on Iranian ports, and Iranian attacks on U.S. military targets in the region. Following the spring decline from above $107 to $67, traders were no longer willing to restore a large geopolitical premium based on headlines alone and were waiting for a visible reduction in physical supply.

Gibson identified ample supply as the principal restraint on prices, citing U.S. production near 13.5 million barrels per day, continued growth in Brazil, Guyana, and Canada, weaker OPEC+ production discipline, and substantial spare capacity in Saudi Arabia and other Gulf states.

He said the more significant upside risk would emerge if the conflict reached Saudi energy facilities or the Bab el-Mandeb. If Saudi refining assets or spare capacity were hit, the current supply buffer could disappear quickly and force the market to reprice crude.

In the short term, Gibson regarded $80 as the key level for WTI. As long as prices fail to break above and hold that threshold, upside potential will remain constrained. A growing threat to Saudi energy infrastructure or major shipping routes could, however, trigger a rapid new advance.

Energy Aspects | Hormuz Traffic Has Fallen Sharply, but Crude Shipments Continue

Christopher Haines, global head of oil at Energy Aspects, said vessel traffic through the Strait of Hormuz had been highly volatile since May. Shipping activity weakened further after the latest military escalation, with vessel flows recording a “substantial decline.”

Haines emphasized that crude shipments were continuing and had not been completely interrupted. The market’s immediate challenge was therefore rising shipping risk and slower flows rather than a total loss of supply.

Hartree Partners | The Market Must Distinguish Disruption From a Higher Risk Premium

Hartree Partners and other energy-market firms said the market needed to distinguish between actual supply disruption and an increase in the risk premium. If the decline in shipping proves temporary, the upside for oil prices could remain limited. If the conflict causes prolonged transportation constraints, the crude market may have to reprice supply risk.

JPMorgan | Lower Refinery Runs Shift the Focus Toward Fuel Shortages

JPMorgan data showed that global refinery runs had fallen by 8.2 million barrels per day in 2026. The decline means that recovering crude supplies may not be fully absorbed by the refining system, increasing the importance of product-market constraints.

The medium-term outlook depends on the restoration of 11.7 million barrels per day of Middle Eastern refining capacity and whether Russia’s refining system can be repaired by early 2027 as scheduled. A slower-than-expected recovery in both regions could prolong structural tightness in refined products and support elevated crack spreads.

Key Crude Oil Market Charts

This section highlights charts that help explain recent moves in the crude oil market, with a focus on changes in supply and demand conditions and market sentiment. The charts and data are based on third-party information and do not represent RYOEX's views or indicate future price movements. Given the risk of sudden market swings, appropriate risk management remains essential.

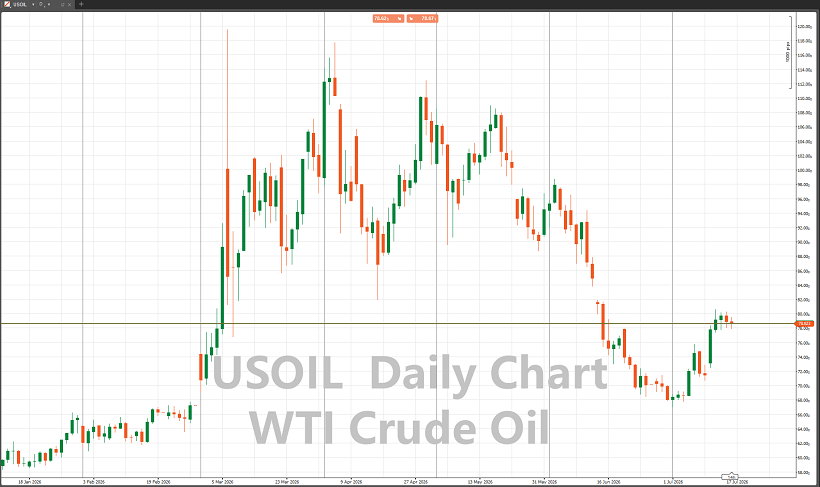

WTI Struggles to Hold Above $80 a Barrel

The chart shows WTI’s repeated failure to sustain a move above $80 a barrel. During Thursday’s session, prices briefly exceeded that level but reversed and settled at $78.88, reflecting traders’ reluctance to price in a larger geopolitical premium without clearer evidence of physical supply losses.

Global Refinery Runs Fall Sharply in 2026

The chart highlights a substantial decline in global refinery runs in 2026. JPMorgan data showed that runs fell by 8.2 million barrels per day, indicating that processing capacity may remain constrained even if crude flows recover.

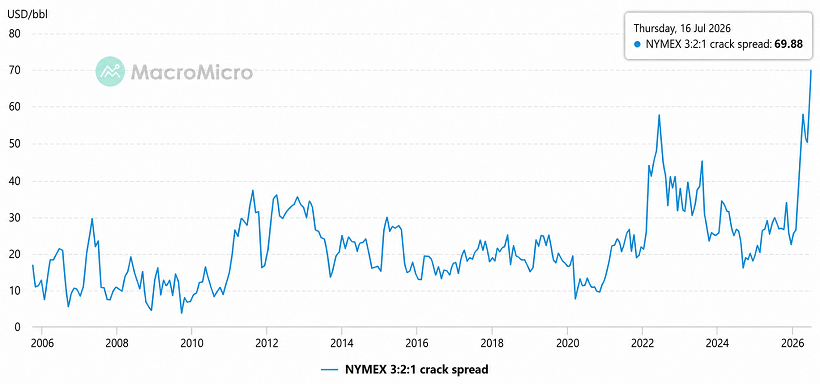

U.S. 3:2:1 Crack Spread Reaches a Record High

The chart tracks the rise in the U.S. 3:2:1 crack spread since the conflict began, culminating in a record high in mid-July. Reduced refining capacity in the Middle East and Russia, together with a roughly two-thirds decline in Russian diesel and fuel oil exports from peak levels, has tightened refined-product markets and allowed fuels to outperform crude.

Summary

Crude prices remain caught between elevated geopolitical and shipping risks and traders’ demand for evidence of actual supply losses before pricing in a larger premium. Hormuz traffic has fallen sharply but has not stopped, while threats involving the Bab el-Mandeb, Saudi energy facilities, and Iraqi export terminals leave significant risks unresolved. At the same time, ample crude production and spare capacity are limiting the upside, while damaged refining systems and lower Russian fuel exports are creating more persistent tightness in refined products. The next immediate catalysts are preliminary U.S. consumer sentiment and inflation-expectations data at 10:00 a.m. ET on July 17 and the weekly U.S. oil rig count at 1:00 p.m. ET.

Enjoyed this article? Share it with your network!

RYOEX Official Media is an information platform created specifically for traders, offering the latest news, analysis, guides, and more. From beginners to experienced traders, we provide useful content to help you stay informed and succeed in your trading endeavors.